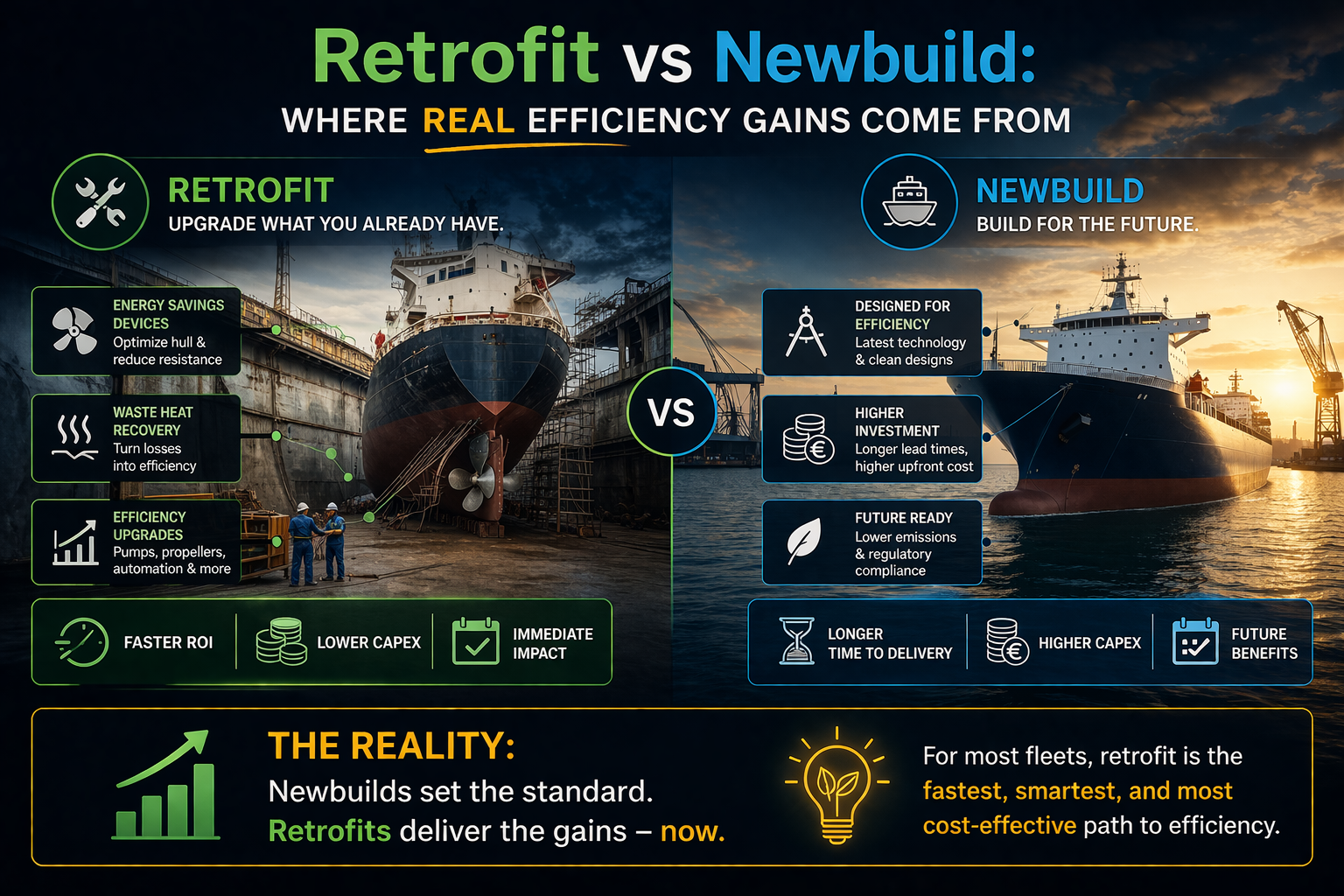

Retrofit vs Newbuild: Where Real Efficiency Gains Come From

EFFICIENCY BEFORE FUEL · SERIES POST 9 · WEEK 16, PART III · APRIL 2026

Why the Existing Fleet Offers Faster, Cheaper and More Certain Efficiency Gains Than Newbuildings in 2026

Maritime Industry | Retrofit Economics | Strategic Intelligence Brief | René Grywnow, DBA

The efficiency gains that matter most in 2026 will not come from vessels ordered today and delivered in 2028. They will come from the 95% of the world fleet that is already at sea, vessels with sub-optimal hull forms, inefficient propellers, oversized pump systems, and energy losses that proven retrofit technology can eliminate within a drydock cycle. The newbuild orderbook is a long-term strategy. The retrofit programme is a 2026 decision.

EXECUTIVE SUMMARY

Lloyd's Register (2025) and ABS (2025) data confirm: propeller and ESD retrofits deliver 3–10% fuel savings per measure; combined drydock packages achieve up to 20%. Demand for energy-saving devices has risen fourfold since 2020, driven by CII compliance pressure and EU ETS cost exposure.

Retrofit packages deliver payback in under three years; dual-fuel newbuilds require 8–12 years under base-case bunker price assumptions, and carry infrastructure dependency risk that retroactively extends that payback further in adverse scenarios.

Retrofit capacity in China has expanded substantially through 2025/2026, reducing yard lead times for combined packages. Owners waiting for newbuild delivery slots in 2028 or beyond are deferring the most cost-effective efficiency window currently available in the market.

1. The Retrofit Advantage in Numbers

The efficiency case for retrofitting the existing fleet rather than waiting for newbuilds rests on three compounding advantages: speed, economics, and certainty. None of these advantages is marginal, each represents a structural superiority over the newbuild alternative in the 2026 decision environment.

Lloyd's Register's Energy Saving Devices Retrofit Report (2025) documents a fourfold increase in ESD demand since 2020. The driver is not idealism, it is arithmetic. CII ratings entered force in January 2023; EU ETS shipping obligations began in January 2024. Every vessel that has not completed a drydock efficiency package is accumulating compliance cost at a rate that no future newbuild can retroactively offset. The economic pressure is real-time and escalating.

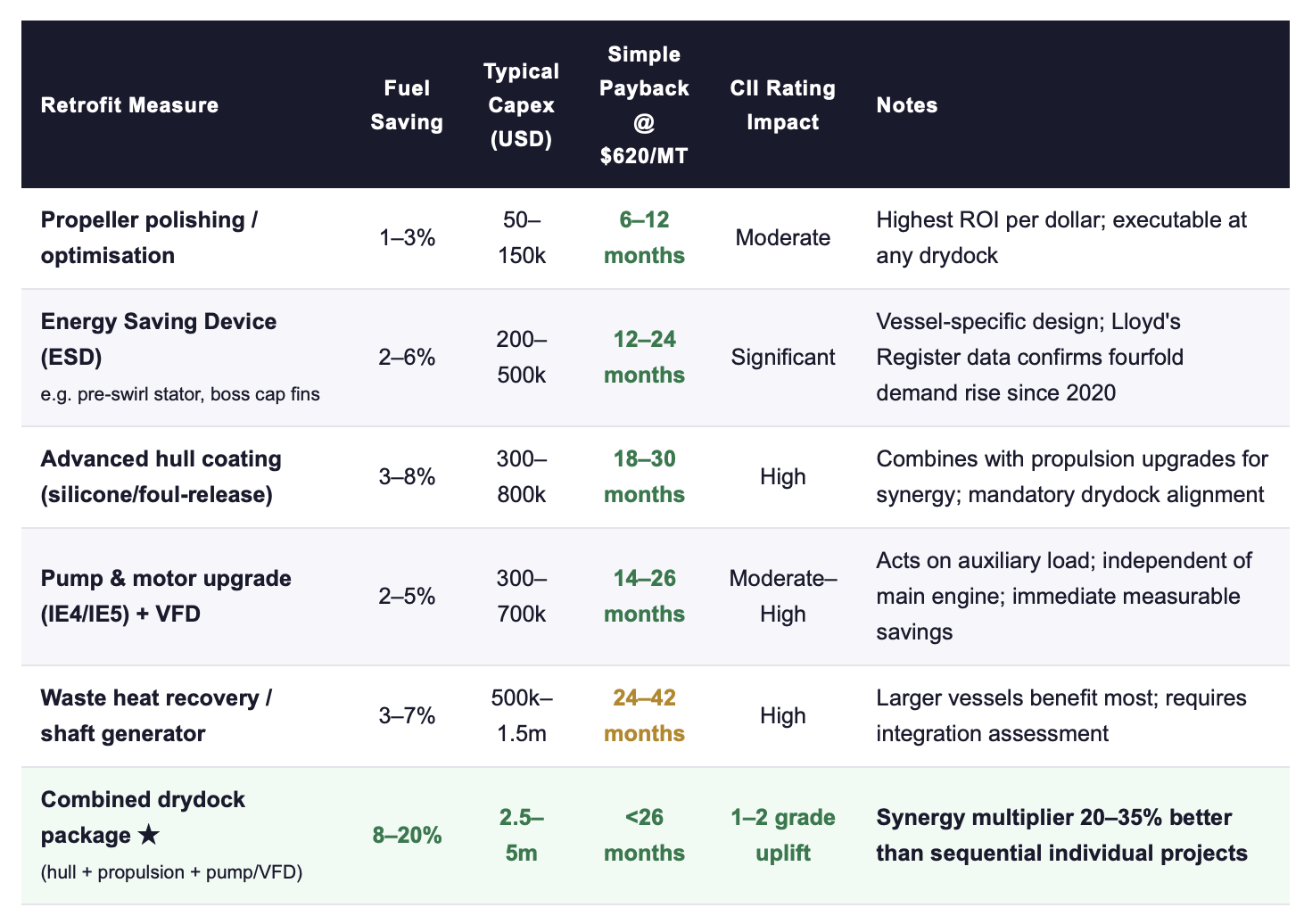

For a single Aframax tanker, propulsion upgrades alone, propeller optimisation, shaft seals, rudder bulb, can deliver fuel savings of 5–8%, which at 2026 bunker price levels translates to approximately USD 3 million over ten years in direct OPEX reduction, plus EU ETS cost avoidance on the same consumption baseline. ABS (2025) data confirm this range across vessel classes and trade patterns.

Sources: Lloyd's Register Energy Saving Devices Retrofit Report, 2025; ABS Retrofits for Energy and Emissions Improvement, 2025; Wärtsilä, 2026. Capex and payback ranges for mid-size bulk carrier / tanker reference vessel.

The table reveals two patterns that most investment analyses miss. First, the synergy effect of combining measures is non-additive, individual measures compound on each other when executed in a single drydock event, producing total savings that exceed the arithmetic sum of individual improvements by 20–35%. Second, even the lowest-return measure in this table, propeller polishing at USD 50–150k, delivers a payback period that no newbuild investment can approach. The economic hierarchy is unambiguous at every price level.

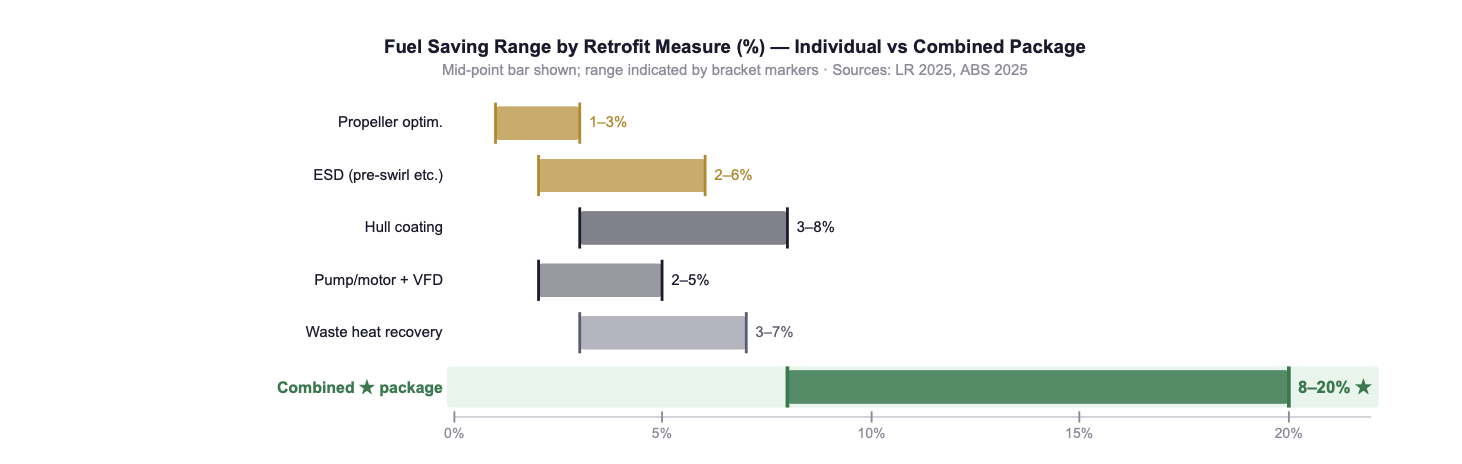

Fig. 1: Fuel saving ranges by retrofit measure. Brackets show min–max; bar width represents the range. Combined drydock package (highlighted, green) achieves 8–20% through synergistic bundling. Sources: LR, 2025; ABS, 2025.

👉 Key Insight: Every measure in the retrofit menu outperforms the newbuild payback timeline individually. The combined drydock package outperforms it by an order of magnitude. The question is not whether to retrofit, it is which measures to bundle, in which sequence, in which drydock window.

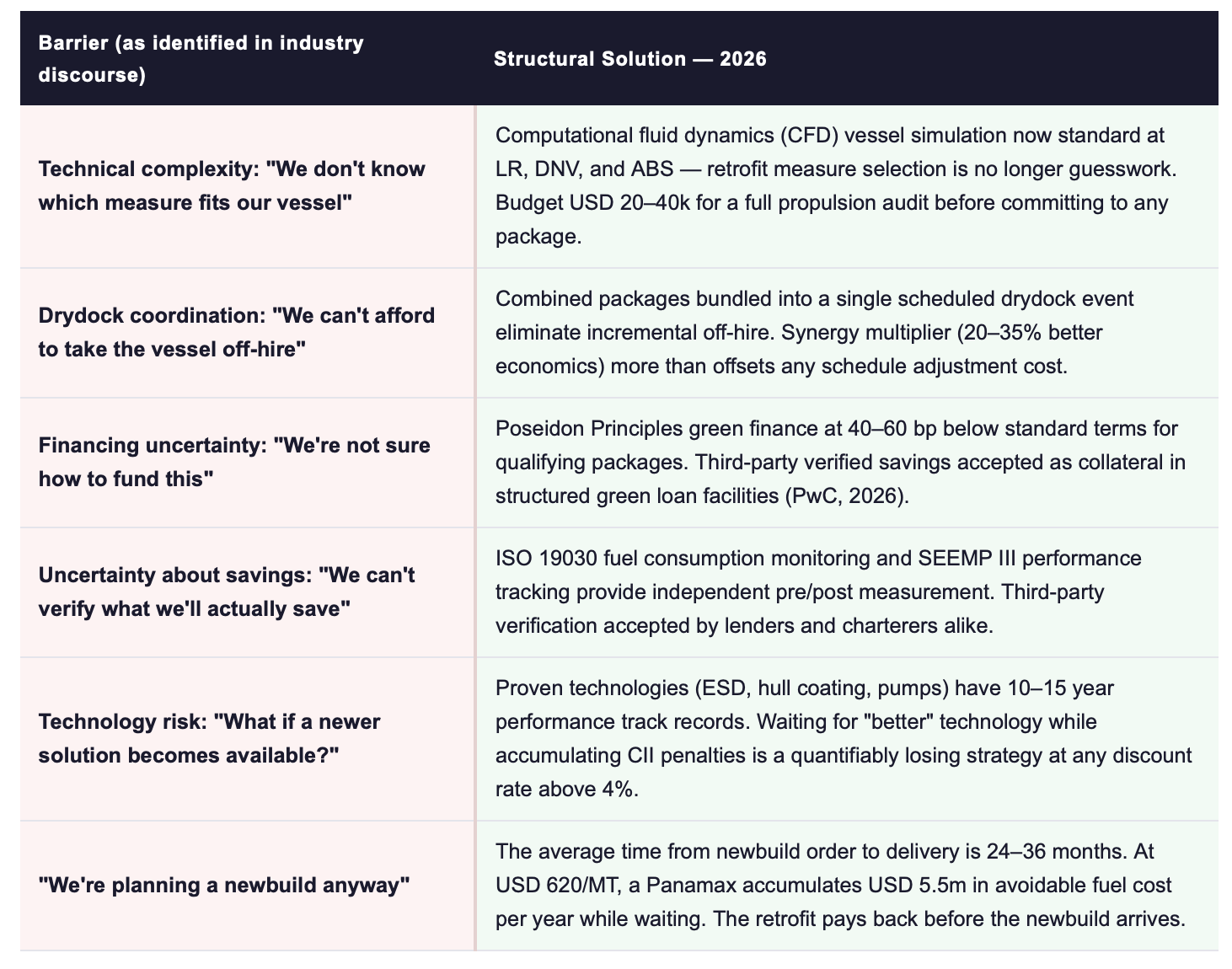

2. Barriers and Solutions: Why "Wait-and-See" Is the Most Expensive Position

The Lloyd's List Shipping Podcast episode "How to retrofit a more efficient shipping industry" is valuable not for confirming the economics, those are well-established, but for documenting exactly why capable operators with available capital still delay. The barriers are real. They are also, without exception, solvable, and the cost of not solving them is now quantifiable in CII penalties, EU ETS exposure, and lost charter premium.

Barrier categories synthesised from Lloyd's List Shipping Podcast ("How to retrofit a more efficient shipping industry", 2025/2026) and ABS industry engagement documentation, 2025.

The "wait-and-see" position has a precise cost. At USD 620/MT and a CII penalty schedule escalating from 2025 through 2030, a Panamax operator who defers a combined drydock retrofit by 24 months accumulates approximately USD 5.5 million in avoidable fuel spend and CII-related compliance cost, before any EU ETS exposure is calculated. That figure exceeds the Capex of the retrofit itself. Waiting is not a conservative position. It is the highest-risk position available.

👉 Key Insight: The barriers to retrofit are real but solvable. The cost of each barrier is bounded and manageable. The cost of not solving them, in accumulated fuel spend, EU ETS liability, and lost charter optionality, is open-ended and growing. "Wait-and-see" is only rational if the cost of the barrier exceeds the cost of inaction. In 2026, it does not, for any barrier on this list.

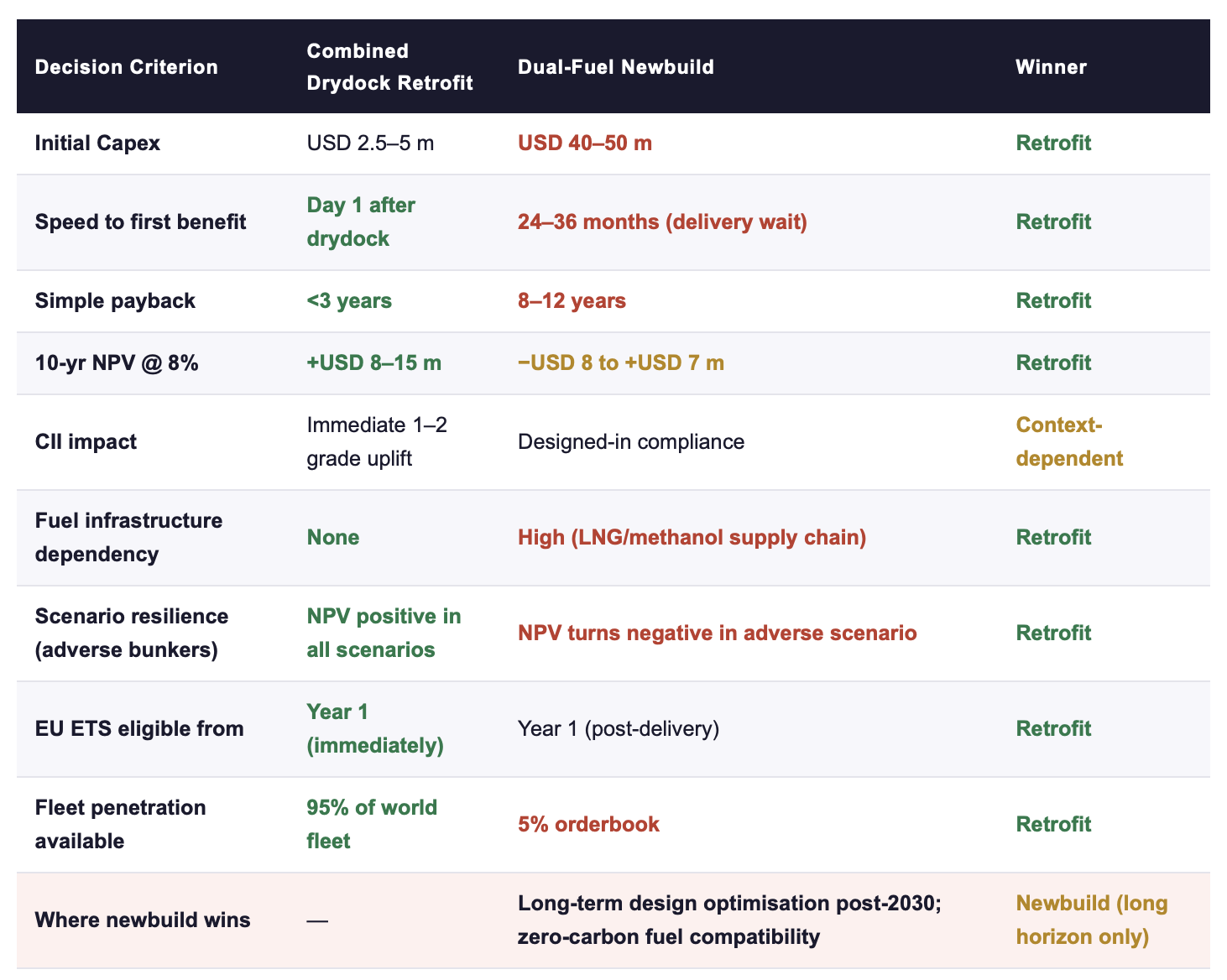

3. Retrofit vs Newbuild: The Complete TCO Comparison

The comparison between retrofitting an existing vessel and ordering a new one is often framed as a technology debate — older design versus newer design efficiency. That framing misses the point. The relevant comparison is economic: what does each option cost in total, when does each option start delivering return, and which option is resilient across the range of plausible future scenarios?

Sources: ABS, 2025; LR, 2025; Wärtsilä, 2026; PwC, 2026. NPV at 8% discount rate, 10-year horizon, base-case VLSFO $620/MT.

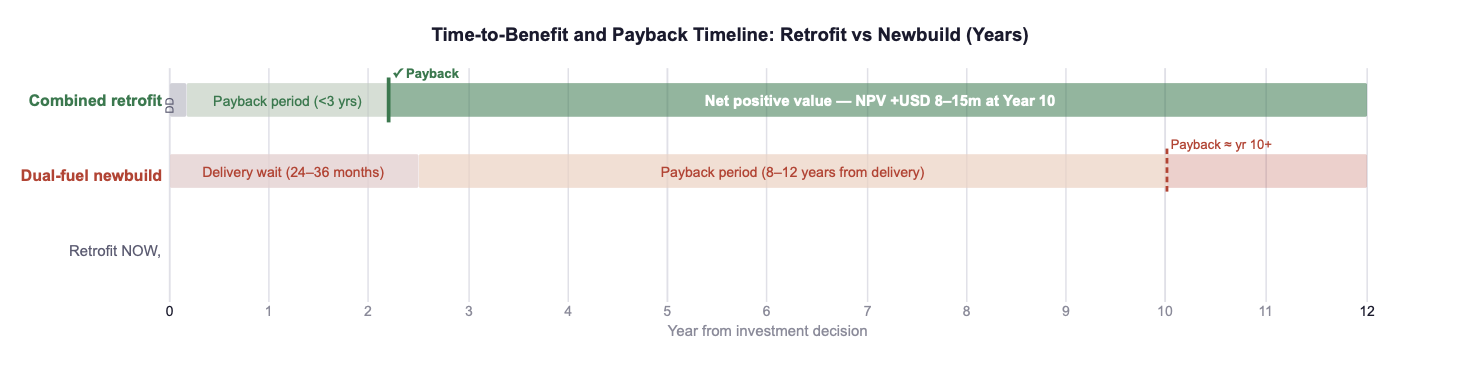

Fig. 2: Timeline comparison from investment decision. Retrofit delivers benefit immediately after drydock; newbuild requires 24–36 months wait before any return. Combining retrofit now with a future newbuild order (Row 3) captures both timelines simultaneously. Sources: ABS, 2025; LR, 2025

Row 3 of the timeline chart makes the strategic conclusion explicit: a retrofit decision and a newbuild order are not mutually exclusive. Owners who retrofit existing vessels now and place a newbuild order for 2028 delivery capture retrofit savings across the waiting period, effectively funding a portion of the newbuild programme from efficiency gains. The two decisions are complementary, not competing.

👉 Key Insight: The retrofit versus newbuild debate is a false choice. The correct strategy in 2026 is retrofit the existing fleet now, capture the savings during the newbuild waiting period, and allow those savings to contribute toward the financing of the next generation asset. The cost of the "newbuild only" strategy is the accumulated fuel and compliance spend during the delivery wait, which, for a Panamax, exceeds USD 10 million over 24–36 months.

4. The 2026 Window: Capacity, Timing, and the Cost of Delay

One element of the retrofit case that has shifted materially since 2023 is supply-side capacity. The narrative that retrofit is constrained by yard availability, which had some validity during the 2021–2023 drydock backlog, has been overtaken by events. Retrofit capacity in China has expanded substantially through 2025 and into 2026, reducing lead times for combined packages at competitive yards.

The practical consequence is that an owner who makes a retrofit decision today can plan a combined drydock event within a realistic 6–12 month horizon, well within the current CII rating cycle and before the 2027 tightening of CII reduction factors. This timing alignment is not a coincidence; it reflects deliberate investment in retrofit infrastructure by Chinese yards anticipating the demand wave that CII enforcement and EU ETS costs are generating.

The cost of delay is now quantifiable with precision. For a Panamax at USD 620/MT with a current CII C rating: each 12 months of retrofit deferral accumulates approximately USD 2.75 million in avoidable fuel spend, plus an estimated USD 0.4–0.8 million in EU ETS compliance cost on that fuel volume, plus the charter rate differential between a CII C and a CII B-rated vessel (estimated at 1–3% on freight rates in current progressive charter programmes). The total avoidable cost of a 12-month deferral is in the range of USD 3.5–4.5 million, against a retrofit Capex of USD 2.5–5 million. The mathematics of delay are definitively negative.

👉 Key Insight: The 2026 retrofit window is the most favourable since CII enforcement began: yard capacity is available, technology is proven, green financing is accessible, and the compliance cost of inaction is at its highest. That combination will not persist indefinitely. Owners who act in 2026 capture the maximum competitive separation. Owners who wait accumulate costs that no future action can retroactively recover.

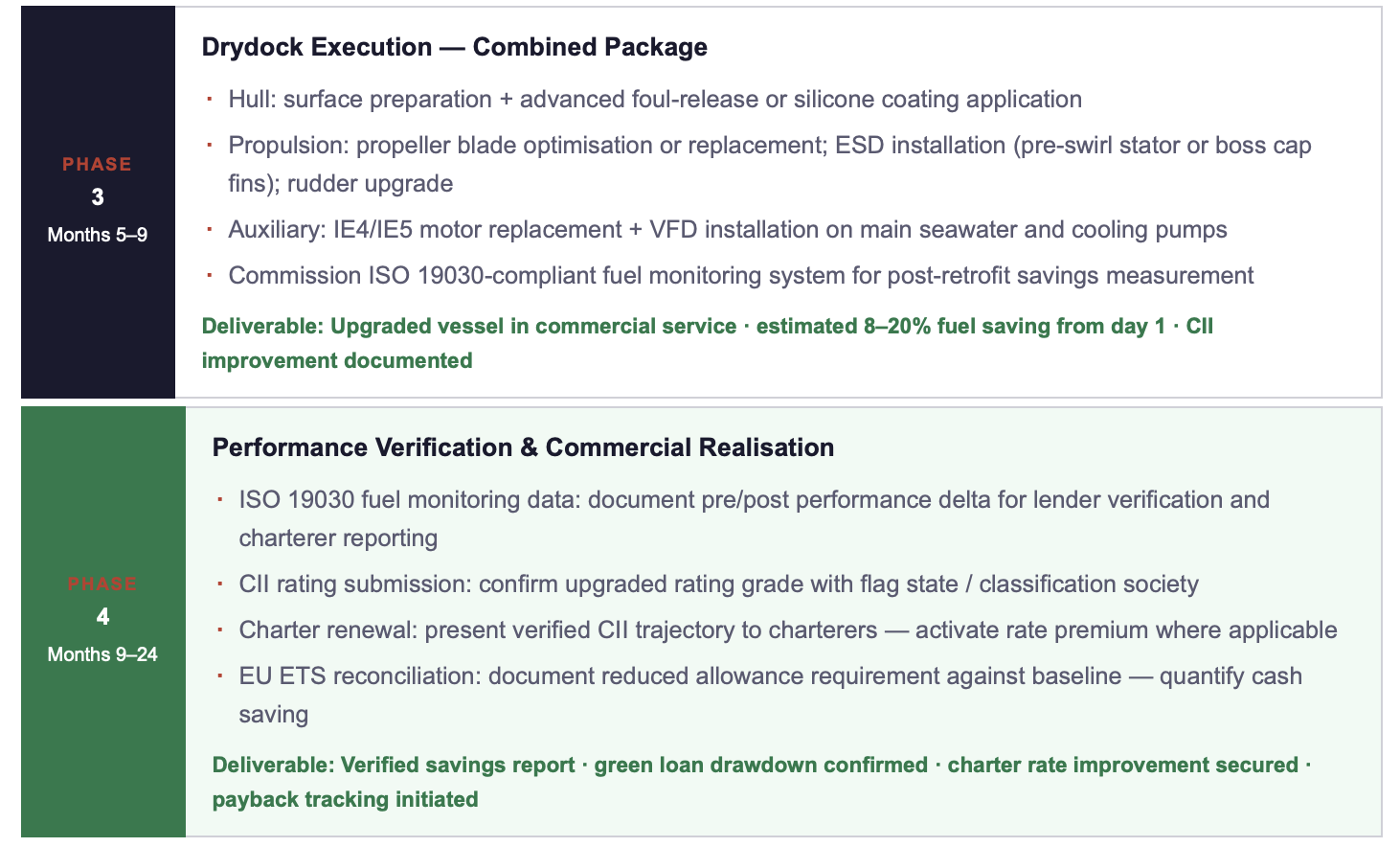

5. Practical Retrofit Roadmap: From Decision to Drydock

The following roadmap consolidates the decision sequence for a combined drydock efficiency package from initial assessment through SEEMP III integration and financing close. It is designed for use in internal planning, board presentations, and technical management briefings.

👉 Key Insight: From decision to commercial operation, the complete combined retrofit roadmap takes 9–12 months. A newbuild takes 24–36 months to the same point, and delivers no savings during the waiting period. The roadmap above is not a theoretical ideal; it reflects current yard lead times and financing structures available in 2026. The execution risk is manageable. The execution value is significant. The execution window is now.

ACTION RECOMMENDATIONS

IMMEDIATE MEASURES (0–90 DAYS)

Commission a propulsion audit for every vessel scheduled for drydock in the next 18 months, identify the specific retrofit package (ESD type, hull coating specification, pump/VFD scope) before the drydock window is fixed.

Calculate the cost of a 12-month retrofit deferral for your highest-exposure vessels: fuel spend + EU ETS + charter rate differential, present this figure to the investment committee as the "cost of waiting."

Request indicative retrofit Capex quotes from at least two qualified yards, establish the 2026 yard capacity reality before assuming unavailability is a constraint.

Check the SEEMP III status for every vessel with a CII C/D/E rating, update the improvement trajectory to reflect the nearest drydock opportunity.

STRATEGIC COMMITMENTS (6–24 MONTHS)

Establish a fleet-wide retrofit sequencing plan: prioritise by CII exposure, EU ETS cost, and charter value, identify the vessels where retrofit payback is shortest and execute those first.

For vessels where a newbuild order is planned: do not defer the retrofit. The newbuild waiting period generates USD 2.5–5.5m/vessel in avoidable costs, capture those savings through interim retrofits and apply them toward the newbuild programme.

Develop a green finance facility structure that covers multiple vessels in a portfolio retrofit programme, lenders offer better terms for portfolio deals that demonstrate fleet-wide alignment than for single-vessel transactions.

Integrate ISO 19030 fuel monitoring across the fleet as standard, the savings data it generates is required for lender verification, charterer reporting, and EU ETS accounting.

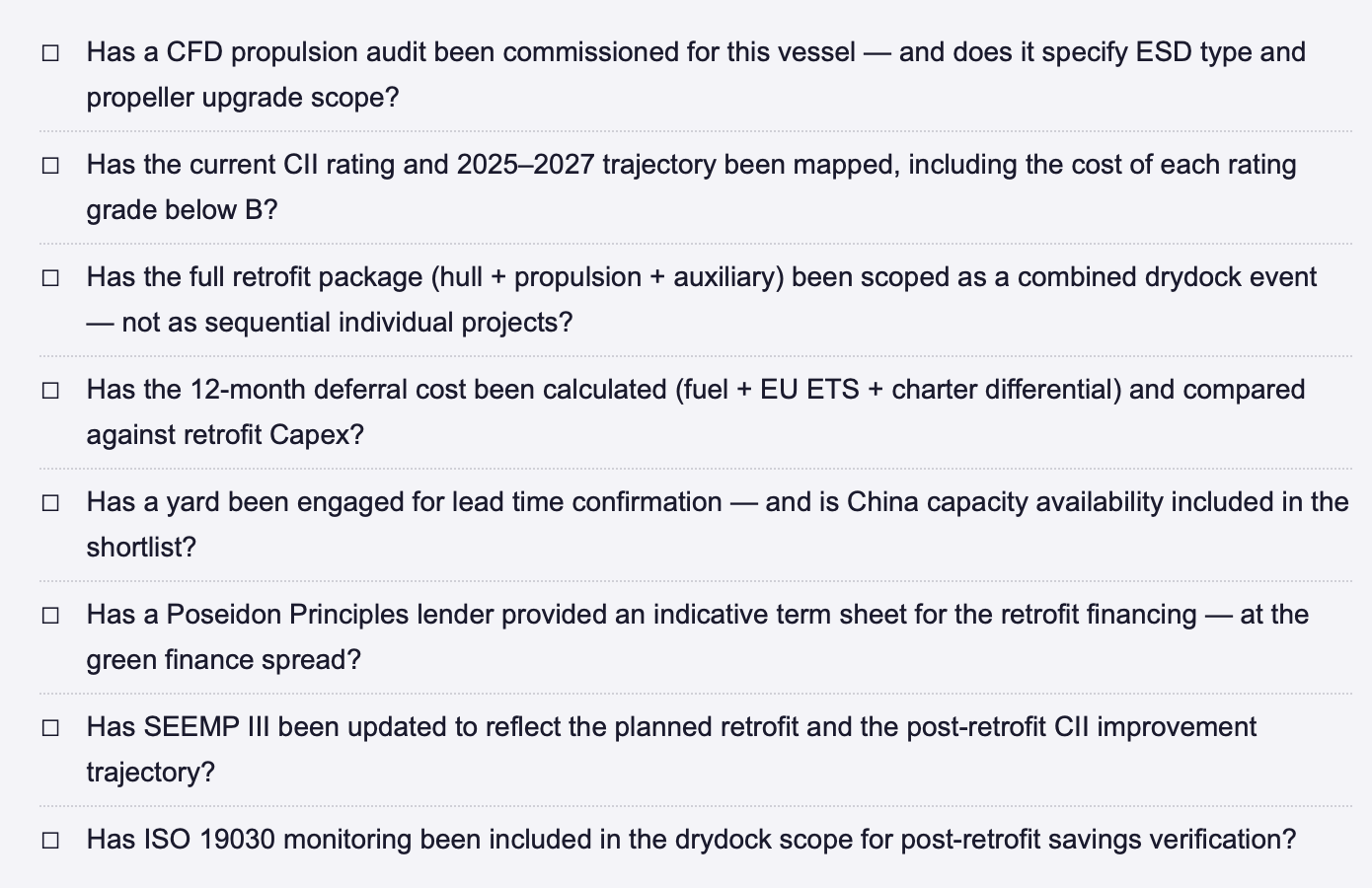

RETROFIT DECISION CHECKLIST, BEFORE THE NEXT DRYDOCK WINDOW CLOSES

FINAL THOUGHT

The 95% of the world fleet that is not in the newbuild orderbook is not a problem to be solved by the next generation of vessel design. It is an opportunity to be captured by the retrofit technologies that exist today, in the yards that have capacity today, with the financing that is available today. The efficiency gains achievable on an existing Panamax or Aframax through a combined drydock package are not incremental, they are transformational in payback terms, in CII compliance terms, and in competitive positioning terms. The newbuild orderbook will eventually renew the fleet. But by the time that renewal is complete, the operators who retrofitted in 2026 will have accumulated years of lower fuel cost, better charter access, and cheaper capital. That is the compounding advantage of acting when the window is open, not when it is optimal in theory.

Where does your fleet stand on the retrofit-versus-wait decision, and what is the specific barrier that has prevented the first combined drydock package from being scheduled? Share your situation for a direct exchange, or connect to discuss the retrofit sequencing logic for your vessel class. | See also: Week 16, Part I (Lifecycle Cost vs Capex) and Part II (Energy Prices as Strategic Risk) for the full economic framework this post builds on.

REFERENCES

ABS (American Bureau of Shipping) (2025) Retrofits for Energy and Emissions Improvement. Houston: ABS.

Lloyd's List Intelligence (2025/2026) Shipping Intelligence Podcast: "How to Retrofit a More Efficient Shipping Industry." London: Lloyd's List.

Lloyd's Register (2025) Energy Saving Devices Retrofit Report: Market Demand, Technology Performance and CII Impact 2025. London: Lloyd's Register.

PwC (2026) Economics of Sustainable Shipping: Green Finance Eligibility, Spread Differentials, and Fleet-Level Risk Modelling. London: PricewaterhouseCoopers.

Poseidon Principles (2024) Annual Report: Portfolio Alignment and Financed Emissions 2024. New York: Poseidon Principles Secretariat.

Wärtsilä Corporation (2026) Lifecycle Optimisation Report: Total Cost of Ownership Analysis for Propulsion and Auxiliary Systems.Helsinki: Wärtsilä.

© René Grywnow, DBA · Strategic Intelligence Brief · April 2026 Efficiency Before Fuel Series · Week 16, Part III

Note: This article reflects my personal views based on industry experience and publicly available information. It does not constitute professional, legal, or investment advice and does not represent the views of my employer.